When designing a billing and rating solution, there is a crucial step at the end of the quote-order-to-cash process. After rating usage events and purchases and issuing bills to the customers, the next step is processing payments. This step usually happens with the help of payment gateway providers, allowing processing payment methods and collection through different payment processors.

A Payment gateway included seamlessly into a billing and rating engine can be a very powerful feature since processing payments closes the final gap in the order-to-cash flow. Utilizing a payment gateway is the approach we decided to take when supporting payment collection in Tridens Monetization, and we achieved that by designing our own Tridens Payment Gateway.

Table of contents

Payment Process Flow

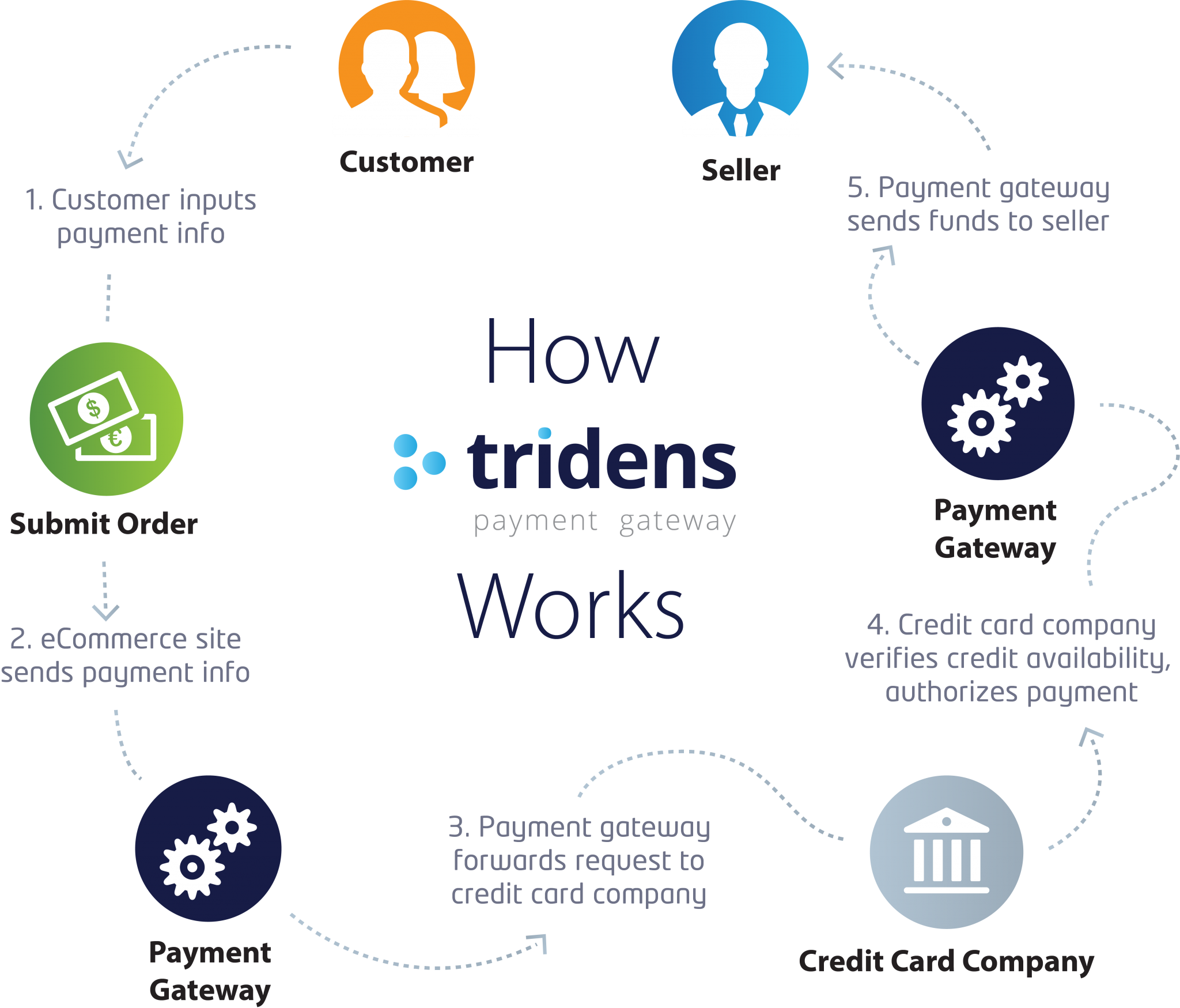

There are several existing payment methods, such as bank transfers, cash payments, SEPA, and card payments. For this explanation, we will focus on the latter, since credit and debit card payments are one of the most commonly used payment methods when processing payments.

Some details may differ among certain industries, but the payment process flow remains quite straightforward for any case:

- The customer has a bill with a due amount, which he decides to pay with a card

- Encrypted card information travels through the payment gateway to the payment processor

- The payment processor checks if this sale is possible by contacting the issuing bank

- The issuing bank can either approve the request or deny it if the customer has insufficient funds

- The payment processor informs you if the sale was successful and informs your merchant bank to credit your bank account

- The only remaining action is the settlement, where the customer’s card issuer ends the actual funds to your account.

The sale consists of two actions, the authorization of funds and the collection of funds. In some industries and use cases, we treat these two actions separately. For example, a customer would like to charge his electric vehicle for 30€. The payment gateway contacts the payment processor to authorize that amount on the customer’s card.

When the session ends, a referenced transaction occurs for those funds to be collected (completing the sale). The collected amount does not necessarily have to be 30€. It can be less due to the customer’s electric vehicle filling up before reaching the limit.

Designing the Payment Gateway

We quickly realize that to support processing payments in our solution, we need to communicate with payment processors, or payment providers as we like to call them. These companies are well known for their payment processing services, which their clients utilize daily for online payment processing. Among such companies are Paypal, Stripe, Authorize.Net, Braintree (a Paypal solution), Wirecard, Cybersource, etc.

These providers sometimes differ greatly in the services they offer, therefore attracting clientele with different needs and requirements. When it comes to working with card payments, there are only a few basic operations to support. Taking into account the card payment process, we need to cover the following:

- Tokenization: Converts the card into an encrypted token. Conversion occurs via a secure connection with a payment gateway or by a user-interface form. The customer directly fills out the user-interface form generated in-app

- Authorization: Reserves funds on a card – sometimes also used for Tokenization

- Deposit: Collects reserved funds via a referenced transaction on a previous authorization

- Conditional Deposit – Sale: Combines authorization and deposit – improves the processing speed when possible

- Void: Void an unsettled transaction

- Refund: Void a settled transaction

The below picture shows a high-level overview of how our Payment Gateway works with processing payments, considering the described operations.

Processing Payments with Tridens Payment Gateway

In one of our previous articles, we talked about integrating Oracle BRM with various payment providers (Oracle BRM Integration with Payment Providers) for processing payments. The Tridens Payment Gateway solution, which we used, was initially designed as a part of our own Tridens Monetization.

The Tridens Payment Gateway is a separate component for communicating with different payment providers offering payment processing services. It supports all the required operations to communicate with third-party services for credit cards, debit cards, and other payment methods by offering a unified set of requests and responses and translating them based on the specifications of each provider.

The Tridens Monetization holds payment method tokens encrypted in a mobile app or via an integrated form before entering our system, which at the same time works towards achieving the 12 requirements to comply with PCI-DSS. Each of our clients in the Tridens Monetization can configure his set-up to work with different payment providers – Wirecard, Braintree (a Paypal Solution), Paypal, Stripe, Authorize.Net, Cybersource, etc.

Below is an example of the communication process.

Conclusion

By designing the Tridens Payment Gateway as a separate component for processing payments, we can also use it as a standalone service and integrate it into other systems. The approach of unified requests and responses allows fast development of specific payment provider features, and even adding new payment providers is not a difficult task. The ability to quickly develop integrations with additional payment processors is imperative when you have a product such as Tridens Monetization. Tridens Monetization serves clients from various industries with customized needs and requirements. The variety of needs and requirements occurs either due to different use cases or due to locale since not all payment providers offer services in the same countries.

Want to get more information about our solutions? Leave a comment below or Schedule a Demo!